C-Corp Basics

The C-Corporation is the default corporate form, meaning when you incorporate your enterprise as a corporation, you are automatically classified as a C-Corp in the state where you incorporate. The C-Corp is generally considered the preferred entity type for businesses that seek funding from sources such as angel investors and venture capitalists. But the tax treatment of C-Corps is often considered the main disadvantage of forming a C-Corp. Additionally, there are significant formalities that must be followed for C-Corps. Below is a description of the C-Corp form in terms of the 4 factors to consider when choosing a business entity. We encourage you to read this article if you are deciding whether you should incorporate your business in Delaware or California.

Limited Liability

The owners of all types of corporations, including C-Corps, enjoy limited liability. As explained in a previous article, limited liability status generally protects the owners of a business in the event that something goes wrong, such as an action that results in injury to a third party. This is often the primary reason to establish a formal entity. Without limited liability, as in a general partnership, the personal assets of the owners (i.e. shareholders in the case of a C-Corp) are available to creditors of the enterprise if the assets of the corporation itself cannot satisfy the debts.

Tax Treatment of a C-Corp

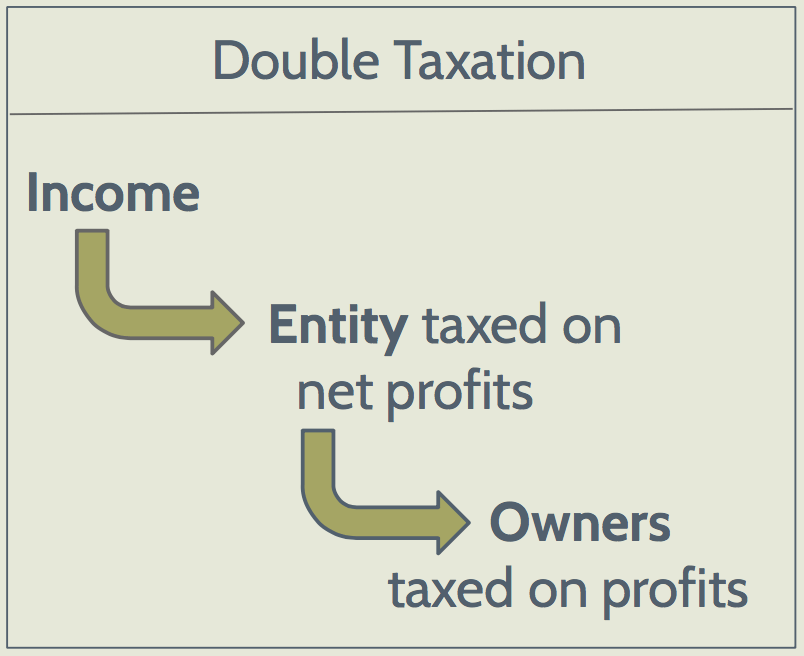

Perhaps the most significant disadvantage of choosing the C-Corporation as the entity type for your enterprise is that it is subject to "double taxation." This means that the net profits (i.e. the portion of income after expenses are subtracted) of the enterprise is taxed once at the entity level, and then the shareholders each pay tax on their individual portions of profits from the enterprise. While double taxation can be a major downside to operating as a C-Corp, it often does not significantly come into play for young companies where expenses (including salaries of employees and payment to independent contractors) tend to "zero out" the balance of the enterprise's bank account.

One option available to enterprises looking to form as a corporation without being subject to double taxation is to elect to be taxed as an S-Corporation by filling out this simple form. When the S-Corporation election is filed, all of the corporation's profits and losses will pass through to the individual shareholders, who claim the profits and losses on their personal income. But there are significant restrictions on when an enterprise can make the election to be taxed as an S-Corp.

At times, it may make sense for a young startup to operate as an S-Corp until it is ready to raise funding from professional investors, who will generally require that the entity be a C-Corp, at which point it can easily revoke the Chapter S election and go back to the default of operating as a C-Corp. By doing this, founders can claim the early losses associated with getting the enterprise off the ground on their individual tax returns to decrease their tax basis. There are some tradeoffs with this approach, so it should only be followed after careful consideration with the help of tax and legal counsel.

Sources of Funding

One of the advantages of operating as a C-Corp is that it is the most flexible entity form in terms of the ability to bring in a wide array of sources of funding, and because it is the preferred entity type for professional investors such as angels and VCs.

The C-Corp is the preferred entity type for institutional investors for a few reasons. First, and most importantly, investors are familiar with the statutes related to corporations and their treatment as shareholders is predictable under these rigid statutes. This is in contrast to LLCs where the rights of owners can vary significantly from one company to the next. Unlike in an LLC, an investor in a C-Corp can know with certainty what her rights (including, for example, economic, voting, and information rights) will be as a shareholder of the corporation. Second, C-Corps can create different classes of stock with varying rights, and institutional investors generally seek "preferred stock" to protect their investment. S-Corps, on the other hand, can only have one class of stock: common stock. Third, stock in C-Corps is generally considered a liquid asset that can be transferred easier than other types of ownership interests.

Formalities

The C-Corp is a formal entity type--meaning that there are strict requirements on how the corporation must be governed. Although a corporation is easy to form by filing Articles of Incorporation (for California corporations) or a Certificate of Incorporation (for Delaware corporations), the ongoing internal governance requirements are strictly mandated by statutes that are specific to the state where the corporation is incorporated. If the owners of the C-Corp do not follow these requirements, they face the risk of losing their limited liability protection (a concept known as "piercing the corporate veil"). Thus, it is important for owners to strictly comply with the statutory requirements for corporate governance, as well as the requirements required by the corporation's charter documents (i.e. bylaws and articles or certificate of incorporation). These governance requirements include, for example, required meetings of shareholders, notice requirements for shareholder meetings, voting procedures, requirements for the composition of the board of directors, procedures for electing and removing directors and officers, requirements for issuance of stock and stock certificates, and others.

Because of this, it is important for founders of a corporation to thoroughly understand the governance requirements associated with forming a corporation. Founders should also take special care to ensure that their formative documents include important provisions that may limit the protections available to owners, such as indemnification rights and limitations of liability for directors and officers.

Are Benefit Corporations and Flexible Purpose Corporations C-Corps?

We have been asked by several social entrepreneurs how the C-Corp vs. S-Corp distinction plays into choosing to form a social enterprise as a benefit corporation or flexible purpose corporation. The answer is that the C-Corp vs. S-Corp distinction is a tax distinction, not an entity type distinction. Thus, by default, a social enterprise formed as a benefit corporation or flexible purpose corporation will be taxed as a C-Corp. But a benefit corporation or a flexible purpose corporation can elect to be taxed as an S-Corp in the same way that a "normal" corporation can.

Contact us to discuss whether a C-Corp will be a good fit for your business.

DISCLAIMER: The information in this article is provided for informational purposes only and should not be construed or relied upon as legal advice. This article may constitute attorney advertising under applicable state laws.

Categories

Recent Posts

- Negotiating Side Letters in Pre-Seed and Seed Rounds

- Key Terms: SAFEs & Convertible Notes for Pre-seed Funding

- A Guide To Raising Money From Accredited Investors

- Startup 101: Overview of Pre-Seed and Seed Investment

- SPZ Legal's Commitment to Social Impact with Pledge 1%

- Issuing Equity to Service Providers? A Guide to Equity Incentive Plans for Startups.

- A Guide to Navigating the New Beneficial Ownership Information Reporting Requirements

- Unveiling the Power of Venture Debt: A Legal Guide for Startup Founders